COMPASS Version 6.2, 6.3, 6.4 © General Re Corporation 2021 - 2026. All Rights Reserved (created: 2025-05-21 generated: 2026-07-10)

Overview

Flexible Underwriting Systems

Underwriting systems have been a successful part of our services for many years. Close cooperation with our clients and decades of underwriting experience have enabled us to develop systems that have been of considerable influence to the underwriting process over the last few years.

-

COMPASS

An underwriting system to process the majority of policies on the basis of the application form. The system is integrated into a company’s administration system or software and covers all underwriting aspects. It is used at head office, point-of-sale and on the Internet. -

Electronic Underwriting Guide Clue

Our user friendly and fast manual featuring underwriting guidelines for medical and non-medical risks.

The system has been developed in close cooperation with direct offices to ensure that all aspects of day-to-day underwriting were taken into consideration and that the system can smoothly be integrated into an administration environment.

The system can underwrite the whole range of life and health products. All underwriting decisions are stored in databases and can easily be modified to reflect each company’s underwriting rules.

This document contains information about COMPASS only; additional information about all other systems can be obtained on request.

What is COMPASS?

COMPASS underwrites life and income protection benefits and recognises applications which can be accepted immediately as well as those which need to be referred. All applications can be processed automatically by the administration system. Requests for additional evidence or even policy issue can be initiated electronically.

Apart from underwriting features COMPASS also provides a component for recording health data. The recording component is easy to use and comprises intelligent word recognition programs which can recognise even misspelled words, abbreviations and colloquialisms (search program).

Upon completion of the underwriting process, the assessment result is sent back to the administration system via an output interface. The assessment result can be displayed with a visualisation component.

Underwriters can easily customise, adapt and maintain all underwriting rules and health data screens to suit the guidelines and underwriting philosophy of the company through a user-friendly COMPASS RuleManager.

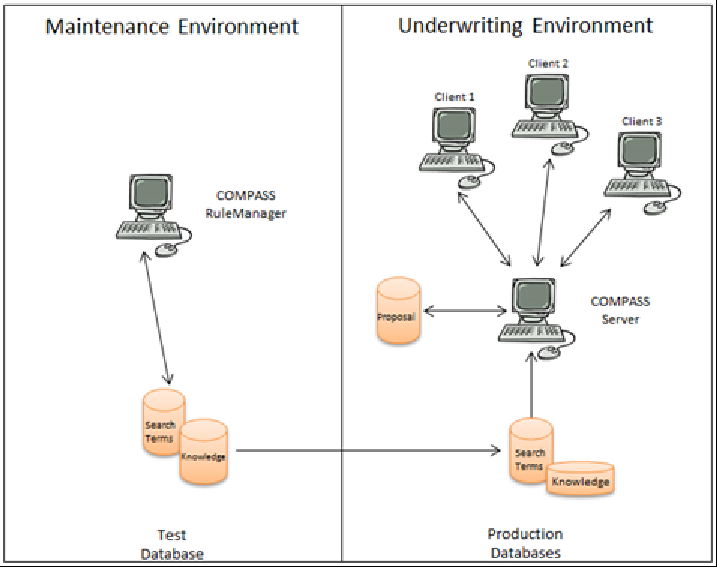

COMPASS consists of an Underwriting and Maintenance environment:

COMPASS Maintenance Environment

The databases containing all the assessment rules can be modified in the maintenance environment. The databases cover the full range of risk factors such as medical disorders, occupations, pursuits and foreign travel.

Gen Re delivers COMPASS with a set of underwriting rules. It includes basic assessments for 25,000 occupations, 15,000 medical disorders, medications, a comprehensive range of pursuits, foreign travel and more. Consequently COMPASS may be used without any major customisation or adaptations. To align the system fully with the underwriting approach and philosophy however, all assessment rules are easily modified using the user-friendly COMPASS RuleManager.

In a typical maintenance environment only a limited number of users – usually only one underwriter – will have access to the COMPASS RuleManager to modify the underwriting rules.

COMPASS Underwriting Environment

Proposals are processed within the underwriting environment. Technical data (e.g. sum insured, duration, age at entry) is transferred via the input interface. The COMPASS data entry component or a data entry component of the company will record the risk data (disorders, general medical questions), COMPASS will do the assessment and the result is displayed by COMPASS or the company’s own program. COMPASS checks the complete proposal taking risk data, legal and technical aspects into account.

This process will be executed in the underwriting environment for multiple users (technically: clients - typically PCs). The clients will request services from the COMPASS server (data-entry, underwriting, display of result, search).

2 separate sets of working environments need to be set up: One complete maintenance and underwriting environment for modifying databases and testing. Another separate set of underwriting environment, without maintenance program, for assessing the applications. For the underwriting environment the data of the maintenance environment is replicated.

Data Storage in COMPASS

Relational databases are used for data storage in COMPASS. A JDBC-interface (Java DataBase Connectivity - driver) is required for the COMPASS database system. It is available for common databases like Oracle, Sybase or DB/2.

COMPASS uses the JDBC interface to access the databases (e.g. underwriting rules for occupations, terms for the result) in the maintenance and in the underwriting environment. The data interfaces (input and output) are implemented with XML.

Versions of COMPASS

Two COMPASS versions are available:

The Head Office Version has been designed for use in the head office or in branch offices. The assessment is based on the information included in a standard application form.

The Point-of-Sale-Version has been designed for use by an agent during a direct conversation with a client, over the counter in a Bank, on the Internet or in a telesales environment. Here the application form is completed using a dynamic dialog tailored to benefit type, sum assured, age, duration and answers to the questions. In addition to the standard application form questions the client may be asked to provide additional information required for the assessment depending on disclosure. The system will prompt for more detailed information, which will be recorded to complete the application process. In this way, the additional queries generated by a simple proposal form can be avoided whenever possible. In most cases the client can be informed of the underwriting decision on the spot.

The dynamic inquiries are described in the Point-of-Sale- Specification.

General Introduction

Scope of Assessment

COMPASS takes into account all life application risks:

-

medical risk

-

occupation risk

-

non-medical risks (nationality, foreign travel, pursuits)

-

financial risk

-

other risks (AIDS-risk, completeness of evidence, etc.)

COMPASS does not only look at individual risk factors, but also takes into consideration potential risks arising through combinations, e.g. occupation and disorders. All individual application details are taken into account for the HIV assessment. The HIV rules do not only involve the beneficiary, but also the occupation, nationality, symptoms of disorders and mode of infection and the relation between the different persons involved in a contract.

COMPASS can arrive at the following results:

-

Standard (including ‘borderline standard’ where a small loading is waived)

-

Offer (percent loadings, per mille loadings, exclusion clauses, reduction in benefit, extended deferred period, etc.)

-

Request additional documents (questionnaire, general practitioner report, etc.)

-

Request information from client (e.g. missing answers in proposal form)

-

Refer to underwriter (e.g. to evaluate documents because of a potentially substandard risk)

-

Defer

-

Decline

Where a potentially substandard risk is suspected additional information (e.g. financial questionnaire, General Practitioner Report) is requested. When a case is referred to a senior underwriter, the system will edit comments to draw the underwriter’s attention to potential problems the system has detected.

This document describes the assessments including the benefit and event related specialities.

Product types handled by COMPASS

A company’s products are termed benefits in COMPASS. Each benefit comprises one or more events (e.g. Endowment Benefits: payment in the event of policy maturity or in the event of death). Benefits and events have individual attributes. A benefit can cover more than 1 person (e.g. joint life applications). Persons are related to events.

COMPASS includes the following benefits; other benefits can be added:

-

Life insurance

-

Pension Plan (Pension)

-

Accidental death benefit (ADB)

-

Income Protection (IP own/similar/any/ADL)

-

Waiver of Premium (WOP own/similar/any/ADL)

-

Total Permanent Disability (TPD own/similar/any/ADL)

-

Critical Illness (CI)

-

Long Term Care (LTC)

-

Hospital & Surgery benefits (H&S)

-

Debility – only available in single markets

-

Dismemberment (DMM) – only available in single markets

-

Business Expenses (BE) – only available in single markets

-

Sickness - only available in single markets

The following attributes specify the benefit:

| Attribute | Value |

|---|---|

Type of benefit(ID) |

|

Benefit name |

|

Smoker type |

Smoker |

Non-Smoker |

|

General |

|

Life policy type |

Joint Life 1. Death |

Joint Life 2. Death |

|

Single Life |

|

Unknown |

|

Life basic form |

Term insurance |

Endowment |

|

Unit-linked Life insurance |

|

Whole Life |

|

Backup-benefit-type-1 (free) |

|

Backup-benefit-type-2 (free) |

COMPASS recognises the following events, when the insurance benefit has to be paid:

-

Death

-

Maturity (Life)

-

Accident (Accident)

-

Disability own/similar

-

Disability any/ADL

-

Critical Illness (CI)

-

Medical care/Long Term care (LTC)

-

Hospital admission and surgery (H&S)

-

Sickness

Events are related to a person. The following attributes specify the event:

-

Event type (ID)

-

Sum insured (e.g. for endowments.)

-

Annuity sum (e.g. for IP annual benefit)

-

Benefit payment period

-

Insurance period

-

Bonus level

-

Waiting period

-

Conversion right (y/n)

-

Examination group

-

Age for assessment

-

Age for examination limit

-

Borrowing

-

Lump sum payment (y/n)

-

Special event benefit (y/n)

-

Premium class

-

Annual premium

-

Premium payment period

-

Single premium

-

Included loading per mille

-

Included loading percent

-

Agreed exclusion clause

-

Range of CI conditions

-

Back up event type 1 (free)

-

Back up event type 2 (free)

Some of these attributes are included in relations. Relations have been built to summarise attribute to logical entities (e.g. premium payment) or to define multiple value relations (e.g. related CI cover). Relations are not further described within this document, but included in the technical description.

With these benefits, events and specific attributes all insurance products can be described. The attributes can be used to implement special underwriting guidelines, e.g. waiver or reduction of loadings for unit-linked products.

The following relations have been defined for events and benefits in the current version; others are possible:

| Product | Benefit | Life policy type | Life basic form | Event 1 | Event 2 |

|---|---|---|---|---|---|

Endowment |

Life |

Single Life |

Endowment |

Death |

|

Term insurance |

Life |

Single Life |

Term |

Death |

|

Whole Life |

Life |

Single Life |

Whole Life |

Death |

|

Unit linked life insurance |

Life |

Single Life |

Unit linked life insurance |

Death |

Maturity |

Joint Life |

Life |

Joint life 1. Death |

Open |

Death AP1 |

Death AP2 |

Joint Life |

Life |

Joint life 2. Death |

Open |

Death AP2 |

|

Pension plan |

Pension |

Maturity |

|||

Accidental Death Benefit (ADB) |

Accidental Death Benefit (ADB) |

Accident |

|||

Income Protection own (IP own) |

Income Protection own (IP own) |

Disability own/similar |

|||

Income Protection o/s (IP o/s) |

Income Protection o/s (IP o/s) |

Disability own/similar |

|||

Income Protection any (IP any) |

Income Protection any (IP any) |

Disability any/ADL |

|||

Income Protection ADL (IP ADL) |

Income Protection ADL (IP ADL) |

Disability any/ADL |

|||

Waiver of Premium own (WOP own) |

Waiver of Premium own (WOP own) |

Disability own/similar |

|||

Waiver of Premium o/s (WOP o/s) |

Waiver of Premium o/s (WOP o/s) |

Disability own/similar |

|||

Waiver of Premium any (WOP any) |

Waiver of Premium any (WOP any) |

Disability any/ADL |

|||

Waiver of Premium ADL (WOP ADL) |

Waiver of Premium ADL (WOP ADL) |

Disability any/ADL |

| Product | Benefit | Life policy type | Life basic form | Event 1 | Event 2 |

|---|---|---|---|---|---|

Total Permanent Disability (TPD own) |

Total Permanent Disability (TPD own) |

Disability own/similar |

|||

Total Permanent Disability (TPD o/s) |

Total Permanent Disability (TPD o/s) |

Disability own/similar |

|||

Total Permanent Disability (TPD any) |

Total Permanent Disability (TPD any) |

Disability any/ADL |

|||

Total Permanent Disability (TPD ADL) |

Total Permanent Disability (TPD ADL) |

Disability any/ADL |

|||

Hospital benefit (H&S) |

Hospital&Surgery (H&S) |

Hospitalisation/Surgery |

|||

Business Expenses (BE) |

Business Expenses |

Disability own/similar |

|||

Debility |

Debility |

CI |

|||

Dismemberment |

Dismemberment (DMM) |

Accident |

|||

Medical Care |

Long Term Care (LTC) |

Long Term Care |

|||

Critical Illness |

Critical Illness (CI) |

CI |

|||

Sickness |

Sickness |

Sickness |

For the various benefits, the following special characteristics are taken into account for the risk assessment:

Pension annuity

No overall risk assessment is performed. In the financial assessment, a check is made against the COMPASS assessment limit and a financial information limit. If term assurance is included - generally in the product pension annuity - it has to be transferred as an own basic form.

Unit-linked life insurance

A unit-linked life policy is assessed in the same way as a term policy. The extra premium is obtained by multiplying the required loading by the sum at risk.

IP

Income Protection (IP) is available with waiting periods 4, 13, 26 and 52 weeks and different types of cover (own/similar/any/ADL). A life assured can apply for several IP benefits with different waiting periods. The interface contains two fields for entering the IP duration. The field ‘insurance term period’ is used for the termination age assessment and financial assessment. The field should contain the relevant duration to be underwritten, which is normally identical to the maximum duration. The field ‘benefit payment period’ can be used in the termination age check.

Business Expenses

This cover insures key persons of a company regarding the loss the company suffers from when the life insured is disabled. It is possible to check several business expenses covers with different deferred periods. An assessment with individual fields is possible. For financial aspects only the financial limit check is done, no needs analysis takes place. For the medical check the shortest deferred period is taken into account. The result of each business expenses cover is the same on the tariff level (worst result), the details are depending on the deferred periods.

TPD

Instead of a monthly benefit, a lump sum payment is made in the event of total and permanent disability. The benefits can include different types of cover (own/similar/any/ADL). The benefit is entered with an appropriately calculated pension (capital/duration). While many companies offer TPD cover as part of their Critical Illness benefit, it is being treated as a 'basic form' for systems' purposes.

Waiver of premium

In the event of a claim for disability, the premium is waived for the related covers. Related covers are those who are included in the relation ‘WOP for premium’. WOP is available with different types of cover (own/similar/any/ADL)

Critical Illness

The illnesses covered can be specified in the relation ‘Range of CI conditions’. If there is no entry in the interface field all illnesses are taken into account. In the assessment process, only those illnesses covered in the policy will be taken into account via the entry in the disorder relation ‘Disorder has CI cover’. Alternatively the interface field ‘benefit/event back up’ can be used to mark different CI covers and depend the assessment in any databases on this field.

Hospital and Surgical

Cost for hospital treatment and surgery are covered within this benefit. The assessment does not depend on the daily allowance benefit.

Sickness

After 7 days of sickness the monthly amount is paid up to 2 years.

Single premium

Risk assessment depending on the type of policy applied for. For the overall assessment the sum assured is reduced by the amount of the single premium. As financial assessments, the single premium is checked against COMPASS limits. Single premium can be agreed for all benefits.

Joint lives

Each life is transferred to COMPASS with its own event, according to the Life policy type. The sum assured and Life basic form applied for can be different for each life. Each life assured can take out as many rider benefits as desired. For each event the partial premium must be transferred at the interface.

Index linking

Index linking has no effect on the risk assessment. It is only taken into account to establish the medical limits via special groups in the examination limit database. This has to be done by the companies themselves.

Group Business

Individuals of Group Business can be assessed by the system. The system does not include special logic for Group Business.

IP, TPD and WOP have four types of cover:

-

Own occupation

-

Own and similar occupation

-

Any occupation

-

ADL (Activities of daily living)

These 3 benefits are assessed, depending on their type of cover, to the events Disability own/similar and Disability any/ADL. The following table shows which benefit is assessed according to which Event:

| Event | Benefit |

|---|---|

Disability own/similar |

IP own, IP own/similar |

Disability any/ADL |

IP any, IP any/ADL |

Financial and limits check and risk consolidation are done for these event types, the relevant sums are added together for this purpose.

Risk classification and assessment

Risks are assessed in two ways in COMPASS:

-

Direct assessment

-

Assessment via risk classification and compensation

Direct assessments are used when the amount of data is small and the assessments are not repeated often, e.g. CSP or Limit databases. The assessment via risk classification and compensation is used for large amounts of data when the same assessments are used for similar risk, e.g. disorder or pursuit database.

Risk level and compensation

Risks are classified on an event level (e.g. IP own/similar risk of individual occupations) by determining specific risk levels (e.g. the occupation engineer is a low risk). An assessment is defined for each risk level, e.g. the risk level low triggers the assessment ’standard’ for own/similar IP cover, and all occupations with risk level low are accepted ‘standard‘.

In the maintenance program COMPASS does not use the risk level name low, high, etc., but directly the assessment to produced user-friendly rules, e.g. risk level low is termed standard. These names can be modified with the maintenance program.

The defined assessment is called compensation (direct assessment) of the risk level. It is determined on a benefit level, e.g. for the risk level medium the assessment for IP own can be different to the one for WOP own. For similar benefits the compensation can be the same, e.g. term and endowment insurance.

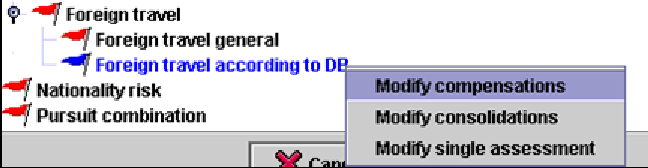

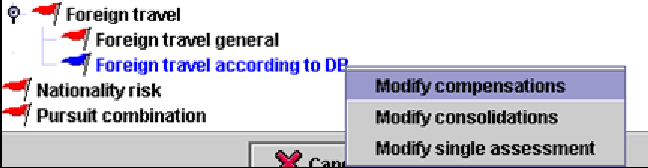

The following paragraphs describe risk levels and compensations using the foreign travel risk as an example. We recommend to start the maintenance program for further information.

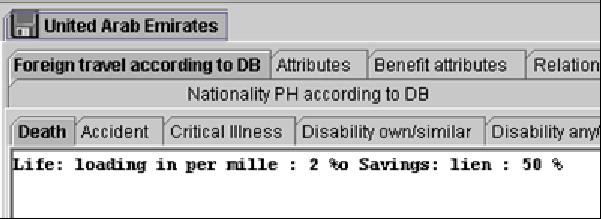

Example foreign travel risk

Via the risk hierarchy the level ‘Foreign travel according to DB’ can be accessed. A right-click on this level opens the menu. The option ‘Modify single assessment’ opens the database editor for the country database including the risk levels for foreign travel. The option ’Modify compensations’ opens the compensation editor of the country database including the direct assessments for the risk levels of the foreign travel.

The option ’Modify compensations’ opens the compensation editor of the country database including the direct assessments for the risk levels of the foreign travel

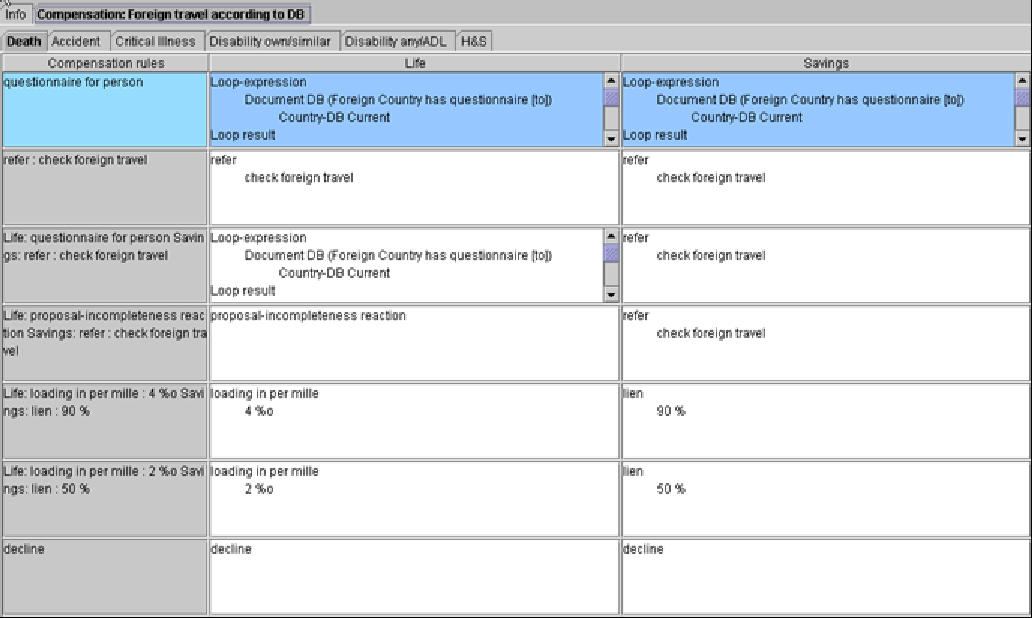

The database editor of the country database includes the event specific risk levels. In this example the risk level name is ’Life: loading in per mille: 2, Savings: lien 50%’ and enables the user to read the direct assessment defined via the compensation editor.

In the compensation editor the direct assessment is defined for every risk level. The left column includes the name of the compensation rule (=risk level), the right columns display the benefit specific assessments. If needed other life products can be defined as separate benefits. The assessments for the available risk levels are done in this editor; it is not necessary to review the complete database.

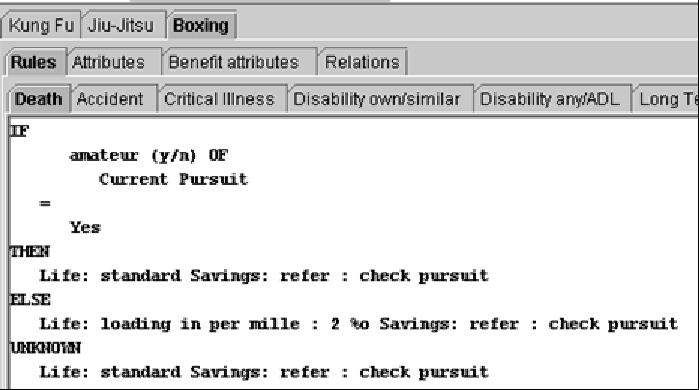

Conditional assessments

The risk classification can be done directly or with conditions. Every interface field can be used as a condition, e.g. amateur status, age for assessment, elapsed time of a disorder. This type of assessment is called ‘conditional assessment’. It has the structure IF-THEN-ELSE. The conditions can be nested.

Compensations

The following compensations are possible for events, others can be defined with the COMPASS RuleManager:

-

standard

-

hint

-

exclusion clause or restricted definition of disability

-

exclusion of

-

extra mortality

-

loading in percent or per mille

-

age increase

-

reduce annual benefit

-

reduce termination age

-

occupation class shift

-

refer with reason

-

request documents (GPR, questionnaire, …)

-

decline

-

defer

-

too unspecific

-

incomplete

Hint: |

Processing of these results is depending on the companies. For substandard risks the various requests can be made before the application is referred to the underwriter. Depending on the nature of the request, the application need only be referred to the underwriter once the outstanding evidence is received. If desired, the suggested loading, exclusion clause, reduction in annual benefit can be sent directly to the agent or broker, or it can be noted as an addendum to the policy.

Assessment results

Scale of assessment results

In our system the individual results have the following meaning:

Standard

An entirely normal risk.

Borderline standard

A slightly increased risk, which is accepted at standard terms in accordance with company policy (business decision - e.g. a loading or further requirements like a medical attendant’s report are being waived).

Accept with loading

An increased risk, for which loading or exclusion clauses are required. However, these are already captured in the proposal and reflected in the relevant premium (e.g. occupational group in IP). Therefore a policy can be issued and there is no need to make an offer.

Offer

As above, but the loading will result in the payment of an extra premium, or an exclusion clause has to be accepted by the client; consequently the client will be given an offer.

Risk data incomplete

Data relevant to the risk (e.g. occupation) is missing in the application. Therefore not all assessments can be completed.

Substandard

The application must be referred to an underwriter. The system may arrive at this result because

-

it has reached COMPASS limits, for example a sum assured limit has been exceeded.

-

it has identified pointers to an increased risk, such as suspicion of AIDS. The system gives specific instructions.

-

further papers must be requested and evaluated by the underwriter, e.g. a doctor’s report or a questionnaire.

-

it has encountered unfamiliar terms, e.g. an occupation not included in the occupations database.

Decline

The risk should be declined. This result tells the underwriter that the application cannot be accepted in its present form. The underwriter should be able to evaluate alternative offers on the basis of the risk factors identified by the system. Therefore each application is evaluated in all areas, even where the reason for decline (e.g. HIV infection) can easily be identified. The underwriter thus obtains a concise overview of all risk-related aspects.

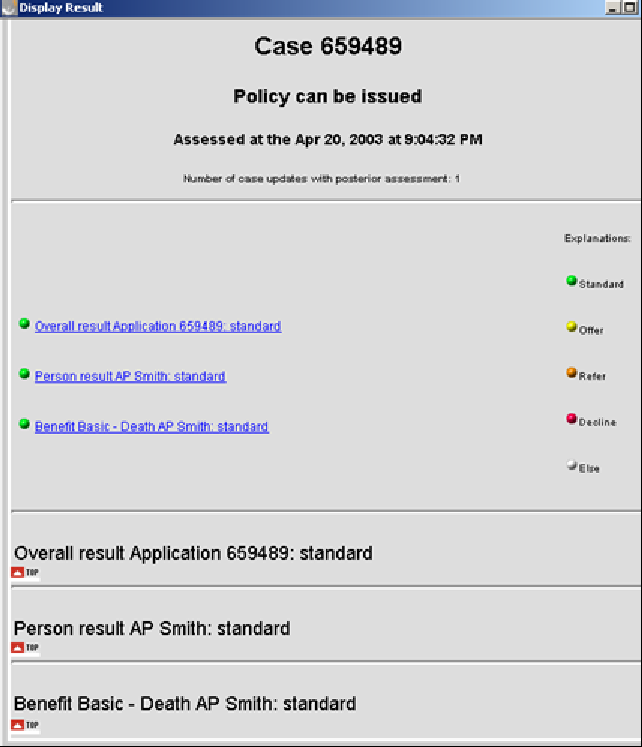

Display of Assessment

The assessment result can be displayed with COMPASS or with a company’s own screens. The output interface includes all information needed to display the assessment. The result displayed in COMPASS is structured in the following way:

-

Header with information about policy issue, application id and point in time for assessment

-

Overview on all partial results without details (overall result, person result, event and benefit result) using colours (green, yellow, red, …).

-

Details for the overall assessment, including the required documents

-

Details for the person check

-

Details for event and benefit results; only the benefit result is displayed if the benefit includes only one event.

For the COMPASS Point-of-Sale – the output has to be implemented by a company. Each company has to decide, which results shall be displayed.

Description of Assessments

Notation

In this chapter the following fonts and sizes are used in the described meaning:

| Font, Size | Meaning | Example |

|---|---|---|

bold, standard size |

Rule name in the maintenance program; important key notes |

Decline suppresses other results |

italic, standard size |

CSP (company specific parameter) |

Association registry reaction GPR |

italic, bold, standard size |

Derived attributes |

Duration consolidated |

underlined, larger size |

Header for rules belonging together, descriptions |

Checking for Completeness |

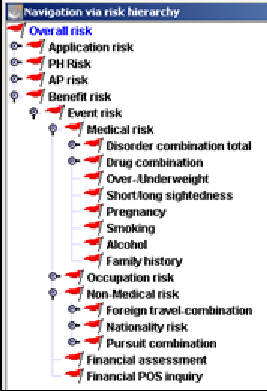

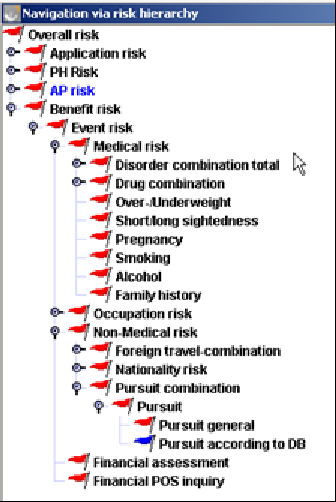

Risk Hierarchy

The following chapters are structured according to the risk hierarchy , which enables the user of the maintenance program to access rules and databases.

The following assessments are currently implemented by Gen Re. Companies can modify, delete or extend the assessments with the maintenance program. Please note that not every risk is assessed for each event. According to the needs, the following checks are carried out:

| Risk | Death | Dis o/s | Dis any/ADL | Accident | LTC | H&S | CI | Remarks |

|---|---|---|---|---|---|---|---|---|

Foreign travel |

yes |

yes |

yes |

yes |

No |

yes |

yes |

|

Nationality |

yes |

yes |

yes |

yes |

yes |

yes |

yes |

|

Pursuit |

yes |

yes |

yes |

yes |

yes |

yes |

yes |

|

Drinking |

yes |

yes |

yes |

no |

yes |

yes |

yes |

|

Smoking |

yes |

yes |

yes |

no |

yes |

yes |

yes |

|

Family History |

yes |

yes |

yes |

yes |

yes |

yes |

yes |

|

Pregnancy |

yes |

yes |

yes |

no |

No |

yes |

no |

|

Dioptres |

no |

yes |

yes |

no |

No |

no |

no |

only for IP and WOP |

Build |

yes |

yes |

yes |

no |

yes |

yes |

yes |

|

Occupation |

yes |

yes |

yes |

yes |

No |

yes |

yes |

if occupation includes occ. Hazard, the occ. Hazard is checked in addition |

Occ. hazard |

yes |

yes |

yes |

No |

yes |

yes |

yes |

|

Medical limits |

yes |

yes |

yes |

No |

yes |

yes |

yes |

If the risk is not mentioned in this table, it is checked for all events.

Overall risk

Obtaining an assessment based on the whole application. The result is always the "worst" result of all the sub-risks, i.e. result per person, per benefit, per policyholder and per application.

Text of the total result

The text of the total result for screen and report file (‘policy cannot be issued’) in the substandard case can be differentiated to

-

‘refer to underwriter’, if there was any direct refer reaction triggered, i.e. not related to the evaluation of an evidence.

-

‘issue evidence’, if missing evidences were the only reason for the referral.

-

‘policy cannot be issued’, if result is ‘offer’ or ‘decline’.

If the same text is used for all listed entries, no difference will be displayed. COMPASS is delivered with the text ‘policy cannot be issued’ for all of these entries.

Request/suppression of evidences

The sequence of these rules is determined with priorities, which can be set for each rule within the maintenance program. For the reader this means, that the rules are processed as listed below.

Decline suppresses other results

The result ’Decline’ suppresses the request of documents and any other inquiries and offer.

Paramedical (medical person who will visit the assured person to check his health)

Paramedicals can be requested via the medical limit database. The CSP GPR instead of paramedical if substandard controls the request of a paramedical if the medical result is substandard. If the value is ‘y’ then a GPR is requested instead of the paramedical. If the value is ‘n’ then the paramedical is requested.

Independent of the medical result a paramedical is suppressed if this is included in the relations of the document category database (see below).

If a Paramedical is requested, the system checks if the applicant has given his consent. If he has not given his consent for a paramedical, a GPR will be requested.

GPR, medical evidence, medical questionnaire suppresses field related incompleteness reaction (client inquiry, step by step, refer because of incompleteness)

If a GPR, a medical evidence or a medical questionnaire is requested for a disorder and, at the same time, a client inquiry is made for the duration of the disorder, the client inquiry will be suppressed (this can happen. e.g. for a different event).

Medical examination already agreed

Once the medical examination limit has been identified, a check is carried out to see if an examination has already been arranged. The agreed examinations are specified in the interface. The scope of those examinations already arranged for (e.g. ME + ECG) is compared with the evidence required as established by the system. If the agreed medical examination equals or subsumes (see suppression logic on evidences) the evidence required, it is noted that ‘examination already arranged’ and no further action is taken. If medical examinations have already been arranged but are not required, the comment ‘medical examination arranged, although not required’ is given and the result is ‘refer’.

The result of every benefit requiring a medical examination will be commented as follows: 'medical evidence is required'.

Evaluate attached documents

The evidence at hand is checked for completeness. Evidence missing will be requested. Evidences to be processed by the underwriter (the attribute ‘existence sufficient’ is not marked in the document database) will be referred to the underwriters with the comment 'evaluate attached documents’.

Previous medical examination available

The existence of previous evidence is checked with the interface. If previously requested documents are available and the previous evidence equals or subsumes (see suppression logic on evidences) the evidence required, the comment 'medical document is already available’ is given, the result is 'refer' and no further reaction is taken.

Suppression of evidences

If different evidences are requested for the same person, it may happen that one evidence is more or less subsumed by another. For reasons of cost minimisation, companies tend to suppress the request of the subsumed evidence in that case. For example a resting ECG may be suppressed by an exercise ECG, or a GPR may suppress a medical questionnaire.

In COMPASS, company specific suppression rules can be set up in the Document and Document Category database:

One document suppresses another

Simple suppression relations can be specified in the Document DB.

Example:

GPRs suppresses the general medical questionnaire for disorders. A hint on the suppressed questionnaire should be given in the result.

For the entry GPR the relation ‘Document suppresses Document with hint’ is set to general medical questionnaire in the Document DB. If no hint shall be given, the relation ‘Document suppresses Document without hint’ has to be used.

A set of documents suppresses another set of documents

Sometimes suppression rules apply not only for a single document but for a set of documents, for example for all client questionnaires. In this case you don’t have to specify the suppression rule for each document. Document categories can be used instead.

The relevant documents are linked to the document category via the relation ‘Document belongs to suppression category’ in the Document DB. In the Document Category DB the relations ‘Document category suppresses Document category with hint/without hint’ include the document category to be suppressed.

Documents can belong to several document categories.

Example:

A GPR suppresses all medical client questionnaires. To specify that suppression rule in COMPASS, follow the steps listed below.

-

Define a document category ‘medical client questionnaire’

-

Relate the corresponding documents (general disorder questionnaire, epilepsy questionnaire, asthma questionnaire etc.) to relation ‘Document belongs to suppression category’ in the Document DB.

-

Specify the relation type ‘suppresses document category with hint’ of the document category GPR with the document category ‘medical client questionnaire’.

A point to note is that the suppression relation is not transitional, i.e. relational chains have to be defined directly.

Please note that the suppression logic is used for the agreed/previous examinations check as well, i.e. the request of one evidence is waived, if there is an agreed/previous examination suppressing that evidence.

Priorities for request of documents

Medical evidences, General Practitioners Report (GPR) and medical questionnaires are requested simultaneously, unless they are suppressed via the document category database. Questionnaires from non-medical risk and financial risk are asked independently on any other questionnaire.

If several medical reports have to be asked for, the GPR is noted as the doctor to be written to, regardless of whether a specialist’s report is to be requested for a particular illness. If only one medical report is needed, the doctor indicated for the disorder is used, if the address is available. If the address is not available, the private medical attendant is written to. If his address is also lacking, the assessment is based on the value of CSP reaction GPR but no doctor. Results can be ‘request a medical examination’, ‘refer with comment ‘GPR required, address not available’ or no special reaction is done. If two GPs are stated in the application form, a GPR is requested from both doctors.

Attached document unnecessary

If the client has enclosed documents, which have not been requested and these are documents to be processed by an underwriter (the attribute existence sufficient is set to ’no’ in the document database), the application is referred with the comment ‘not needed documents’.

Checking for Completeness

The risk-relevant fields of the interface are checked for completeness. For each field an incompleteness reaction is specified in the user interface database with the attribute ’Unknown reaction’, e.g. ’incomplete’, ‘refer’ with the comment ‘incomplete field’, ’ignore’ or ’step by step’. The incomplete reaction is related to the source type, it can be different for several application forms. In the following this reaction is called proposal incompleteness reaction. Rules have to be defined for the application fields to initiate the incompleteness reaction. These rules can use the proposal incompleteness reaction or other reactions can be defined. The access to the proposal incompleteness reaction enables companies to change the incomplete reaction without changing the rule. There are three basic situations where an incomplete reaction for a field is triggered:

1. Static Incompleteness

If fields are unknown, COMPASS reacts according to the rule. This can be an access to the proposal incompleteness reactions or a direct reaction. The kind of the incompleteness check is depending on the use of the field for assessment rules and has to be defined within the relevant risk, e.g. AP or PH. These rules are gathered in the related sub risk plausibility.

2. Dynamic Incompleteness in assessment rules

If an assessment is depending on conditions and these details are not indicated in the proposal, COMPASS processes the unknown part. For example the amateur field may be required to assess a given pursuit. The unknown part can include any reaction, e.g. questionnaire or the proposal incompleteness reaction. The incompleteness reaction is initiated for every incomplete condition. If the condition includes internal attributes and assumptions have to be made for the assessment, the incompleteness check has to be defined in addition within the static incompleteness rules (e.g. annual income).

If the condition includes internal attributes and no assumptions are made if the data is missing, the unknown part is processed (e.g. duration consolidated).

3. Dynamic Incompleteness for connected fields

If a yes/no question needs details, e.g. sidelines (y/n) and the amount and the details are missing, COMPASS evaluates the unknown part. For health questions it can be checked, whether impairments according to the organ category or time period are indicated. This kind of incompleteness check is included within the risk related rules. These rules are gathered in the related sub risk plausibility.

If fields are not needed, i.e. not included within the proposal, at least the combination rules shall be deleted. If additional fields are prompted, the incompleteness rules have to be enhanced.

Hint: |

Each field has an internal code and a name. The name can be modified by the company and does not have to be the same as within this document.

Application risk

The application risk comprises all application related aspects as opposed to the person and event related checks. It consists of application related plausibility checks, formal and legal aspects.

More application data

If the client has provided application details, which cannot be entered, the interface field ‘moreentries’ has the value ‘yes’. In this case the application is referred with the comment 'check un-entered application data'.

Plausibility application

Beneficiary Death

The completeness of the beneficiary is checked. If no beneficiary is indicated, the incomplete reaction for the relevant beneficiary is triggered as for any other incomplete data. If the beneficiary is indicated, it is checked within the AIDS risk (see AIDS risk). Furthermore a check is performed to see whether, in the event of death, a drawing entitlement is indicated for the insured himself. This is the case if the beneficiary is the policyholder, but the policyholder is also the assured person. In this case the application is referred with the comment ‘insured authorizes himself’. Term or whole life benefits are checked as to whether the death beneficiary is indicated. If it is missing COMPASS reacts according the incomplete reaction.

Special agreements

If the question for special agreements is answered ‚yes’ and no special agreements are indicated, a client request is initiated.

Formal risk

Agent check

COMPASS stores the following data on the agent/broker:

-

Name

-

Id no

-

Nationality

-

Agent code

The following checks are processed for the agent:

Agent flag

The agent code is stored in a database with text, which then appears as a comment in the result 'check agent/broker, because'. No further processing is done with this code (e.g. special commission arrangement, new broker).

Agent is premium contributor

If the agent’s / broker’s name is the same as the premium payer’s name and the broker is not the policyholder, the application is referred with the comment 'broker and premium payer are identical'. The agent / broker data is made available to COMPASS via the interface database from the company’s own agent / broker database.

The agent’s nationality is checked within the check for the policyholder.

Relationship between PH and AP

If an AP exists that has specified ‘other’ as relationship to the PH, the application is referred with ‘check relationship between APs and PHs’. This reaction is only executed if the field relationship to PH is used in the input interface. It is executed only once for the application form. See also the chapter ‘special checks for PH’ for other regulations on the relationship between AP and PH.

Legal risk

Missing signatures

If the general question for signatures is answered with ‚no’, the signature is requested from the client.

Missing account holder signature

If the account holder is different as the AP and PH and the answer to the questions for signature of account holder is answered with ‚no’, the signature is requested from the client.

Missing agent signature

If the question for signature of the agent is answered ’no’, the application is referred with a hint on the missing signature.

Deletions

Deletions and amendments in the closing declaration or on the reverse of the application are significant. Applications with deletions are therefore referred with the comment 'deletion/amendment in the closing declaration, or similar.

Telephone Inquiry

If the question regarding telephone enquiry is answered "yes", the result contains the comment 'telephone enquiry - confirm in writing’.

Special agreements

Special agreements are processed with the special agreement database. This database should include those agreements, which can appear quite often in application forms. The database attribute relevant for assessment controls the processing of the special agreements.

Relevant for assessment

If this attribute is set to ‚yes’, the application is referred and the hint ‚check special agreement’ is given.

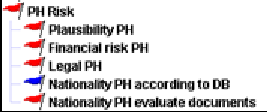

Policyholder risk

The policyholder risk includes policyholder related checks. These checks are only important for the role as a policyholder. The risk consists of plausibility checks, financial and legal aspects and the nationality check.

Life different reaction

If the policyholder is a natural person and is not the life to be assured, the questionnaire Life of another form is requested. See also the chapter Formal risk for possible reactions depending on the relationship of AP and PH.

Plausibility Policyholder

This chapter includes policyholder related completeness checks. The checks are only done if the Policyholder (PH) is not an assured person (AP).

Investment income

If the question for investment income (y/n) is answered with ‚yes’ and/or no amount is given, COMPASS reacts according to the incompleteness reaction.

Occupation

If the sex of the policyholder is male or female and the occupation is not given, COMPASS reacts according to the incompleteness reaction.

Occupational status

If the sex of the policyholder is male or female and the occupational status is not given, COMPASS reacts according to the incompleteness reaction.

Branch of industry

If the sex of the policyholder is male or female and the branch of industry is not given, COMPASS reacts according to the incompleteness reaction.

Physical work

If the sex of the policyholder is male or female and the answer to the field physical work (y/n) is not given, COMPASS reacts according to the incompleteness reaction.

Annual income

If the sex of the policyholder is male or female and the amount of the annual income is not given, COMPASS reacts according to the incompleteness reaction.

Financial risk policyholder

The financial assessment for the policyholder is implemented within this risk. The documentation contains the description of these checks in the chapter Financial Assessment.

Legal risk Policyholder

Signatures

The incompleteness check for the policyholder’s signature is processed, if it is needed:

| Age | Signature requested |

|---|---|

Age < CSP signature_age |

signature of legal representative of policyholder |

Age >= CSP signature_age |

signature of policyholder |

A typical value for signature_age might be 18 years. The system will check the age on the day the application form was signed.

Minor Policyholders

In the financial limit database the benefit group ‘Life: Financial Check for PH’ is reserved for financial PH checks. The sum assured that is used for the test, is the sum of the sums of all benefits with event death. In the limit-database several entries can be made in different age ranges. So every company has the flexibility to decide up to which sums minor policyholders are acceptable. Possible explanation texts for referral are: 'policyholder is a minor’ or 'check sum assured for under-aged policyholder'. Additional documents can be requested. The rules required documents and required hints initiate the request.

Nationality PH according to database

The assessment of the nationality risk for the PH is based on the Country Database. The country database includes a code for any synonym term. The relation 'Region belongs to country' connects abbreviations, towns and regions of a country with the country. The assessment of e.g. single regions can be different.

Nationality cannot be captured

Where '?' is entered for nationality, the application is referred with the comment 'nationality cannot be entered'.

Nationality unknown

A check is made to see whether the database contains any entry at all for the specific nationality. If not, the application is referred with the comment 'policyholder’s nationality not found'. If the policyholder’s nationality is unknown, the incompleteness reaction is triggered if the PH is a natural person.

The PH will be assessed on the basis of his nationality and place of residence. The following assessments have been used within the nationality risk for compensation of the risk level:

-

standard

-

exclusion clause

-

refer with the comment 'nationality to be checked'

-

questionnaire

-

decline

Other assessments, e.g. a request of additional documents (work permission, etc), can be implemented.

Risk level may depend on the following conditions:

-

residence

-

length of residence

Residence

The residence check is done with the internal attribute residence ok for PH. For setting of the internal attribute the value of the country db attribute ’Residence’ is used and checked on adherence. The attribute ‘Residence’ has four values:

-

domestic residence or residence in country of nationality

-

residence irrelevant

-

residence in country group required

-

domestic residence required

The relation ’Country belongs to country group’ determines the membership to a country group. The countries of this country group can be assessed analogue, but individual assessment is also possible.

For a referral the comment 'no matching residence' can be given.

Length of Residence

The length of residence can be checked in addition to the residency.

Nationality PH evaluate documents

This risk can contain overall rules for document requirements for nationality. Currently it is empty.

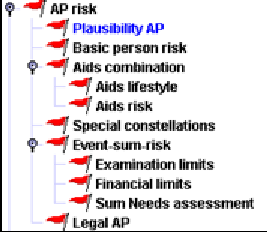

AP risk

The AP risk includes person related assessment, independent on event and benefit. It consists of plausibility check, basic person check, Aids risk, special constellations, legal risk and event sum risk. The event sum risk is created on this level, because only here overall sums for several benefits/events can be calculated, e.g. for limit checks.

Plausibility AP

For the following application fields it is checked, whether the answer is given and if details have been indicated. This assessment is only done, if the fields are part of the application form. If details are missing, the relevant question and a hint on the missing details is given in the result:

-

occupational status

-

branch of industry

-

manual work

-

annual income (amount)

-

foreign travel (y/n)

-

pursuits (y/n)

-

occupational hazard (y/n)

-

excluded from military service (y/n)

-

critical illness in the family (y/n)

-

height

-

weight

-

pregnancy, only if AP is female

-

month of pregnancy, only if required within pregnancy rules

-

drugs

-

diet for medical reasons

-

reduction in earning capacity (y/n)

-

smoking (y/n)

-

ever smoked (y/n)

-

drinking (y/n)

-

ever drunk (y/n)

-

health questions 1

-

…

-

health question 50

-

IP benefit from other sources (y/n)

-

sidelines (y/n)

-

investment income (y/n)

-

Pre-existing policy (y/n)

-

Pre-existing Disability own/similar policies (y/n)

-

Pre-existing life policies (y/n)

-

Pre-existing LTC policies (y/n)

-

Pre-existing Critical Illness policies (y/n)

-

Pre-existing Accident policies (y/n)

-

Pre-existing Disability any/ADL policies (y/n)

-

Pre-existing TPD policies (y/n)

-

Pre-existing H&S policies (y/n)

Hints to all questions

If a question is not used in a source type, the plausibility rule has to be deleted or the incomplete reactions have to be set to ‘ignore’ to avoid an incompleteness reaction. If questions are depending on conditions (to be defined in the user interface db), the conditions have to be repeated within this risk level. Possible conditions are only for IP, only for very high sums insured.

Hints to the medical questions

Answers to medical questions of the AP can be processed as needed according to plausibility and completeness. Processing is person-related, unless a reaction applies to one particular benefit/event. 50 questions (health question 1 to 50) are available for these medical questions. Plausibilities in regard of questions numbers, periods and organ categories can be included.

Examples:

Category 1

When the question is answered with 'yes' and no disorder is given in response to this question, the incompleteness reaction is triggered.

If the question is answered 'yes' and a disorder is stated, the assessment takes the disorder into account.

-

Have you ever undergone psychiatric treatment?

-

Are you suffering from disorders of any other type?

-

Have you ever suffered from any allergies now or in the past?

-

…any infectious diseases now or in the past ?

-

…any viral diseases now or in the past ?

-

…any sequelae of previous disorders, now or in the past?

Category 2

If the question is answered with 'yes' and no disorder is given in response to the specified organ category, the application is referred with the comment 'no disorder given for organ system' or the result is incomplete.

If the question is answered with 'yes' and a relevant disorder is given, the assessment takes the disorder into account.

-

Have you ever undergone surgery?

COMPASS checks if a disorder is given which is coded with the organ category 'surgery'. -

Have you ever suffered accidents, injuries, poisoning?

COMPASS checks if a disorder is given which is coded with the organ category ‘accident, injuries and poisoning’. -

Have you ever had or do you now have any disorder of the respiratory system?

COMPASS checks if a disorder is given which is coded with the organ category 'respiratory system'.

Category 3

If the question is answered with 'yes' and no disorder is given in response to this question, the incompleteness reaction is triggered.

If the question is answered with 'yes' and a disorder is given, the application is referred with the comment 'check disorder to following question'.

-

Are you receiving or have you ever received disability benefits?

-

Are you expecting to be hospitalised?

-

Has a doctor prescribed a special diet for you?

-

Have you ever had X-rays taken?

-

Have you ever undergone medical investigations with abnormal results?

-

Have you ever been institutionalised for alcohol/drug abuse?

Category 4

If the question is answered with 'yes' in response to this question, the incompleteness reaction is triggered.

If the question is answered with 'yes' and a disorder is given, the assessment takes the disorder into account for Life, Accident, H&S and LTC. IP, CI and TPD applications will be referred in any case with the comment 'check disorder to following questions'.

-

Have you given up smoking for health reasons?

-

Have you changed your occupation on health grounds?

Category 5

If the question is answered with 'yes' and no disorder or dioptres are given in response to this question, the incompleteness reaction is triggered.

If the question is answered with 'yes' and a disorder or dioptres are given, the assessment takes the disorder or visual impairment into account.

-

Are you suffering from any medical disorders?

-

Have you undergone any treatment?

-

Do you have any sequelae to health?

Basic person risk

Assessment of pre-existing policy

For application detail and association registry entries it is checked if the policy is with one’s own company. The company is defined with CSP company.

Association registry

The details are taken from the interface data. A check is made to see whether there is any data available on the life to be assured. Independent on the event/benefit, only entries with result substandard are taken into account. It is checked by which company the entry given.

Association registry own company

If the pre-existing policy is with one’s own company, the application is referred with the comment 'pre-existing policy accepted as substandard risk'.

Association registry other companies

If the pre-existing policy is with another company the CSP association registry reaction GPR will determine whether the application is referred with the comment ‘check association registry’ (066) and additionally a GPR is requested.

Association registry company unknown

If the company cannot be found in the company database, the application is referred with the comment 'entry with unknown company'.

Own Portfolio details

The portfolio details are entered in the interface in cumulative form. For every event in the portfolio the following fields may be provided by the administrative system: sum assured to be considered for the financial assessment, sum assured to be considered for the medical assessment and acceptance result (worst acceptance result of all pre-existing policies). The sum of the field with the extension _f, for example sum_assured_f, is used in the financial assessment. The sum of the field with the extension _e, for example sum_assured_e, is used in the evaluation of examination limits.

Own portfolio policy substandard

If the acceptance result from pre-existing policies is ‘substandard’, the application is referred to the underwriter with the comment 'pre-existing policy with substandard result in portfolio’.

Own portfolio policy declined

If the acceptance result from pre-existing policies is ‘decline, the application is referred to the underwriter with the comment 'pre-existing policy declined in portfolio’.

Own portfolio policy incomplete

If the acceptance result from pre-existing policies is ‘incomplete’, the application is referred to the underwriter with the comment 'pre-existing policy incomplete in portfolio’.

Own portfolio policy claim

If the acceptance result from the pre-existing policies is ‘claim', the application is referred to the underwriter with the comment 'pre-existing policy with claim in portfolio’.

Own portfolio policy longstop

If the longstop limit is exceeded, recognized by the interface field longstop, the application is referred and the comment ‘check longstop limit’ is given. A longstop limit is an internal definition of pre-existing insurances.

Application details

Benefit related substandard previous insurances

Substandard, declined or deferred pre-existing policies, which are declared by the life to be assured in the application form (as an answer to the question related to every type of benefit), are referred to the underwriter with the comment 'client indicates pre-existing substandard policy'. Substandard previous insurances at the own company are processed in the same way.

General substandard previous insurances

Substandard, declined or deferred pre-existing policies, which are declared by the life to be assured in the application form (as an answer to the general field for substandard, declined or deferred pre-existing policies), are referred to the underwriter with the comment 'client indicates pre-existing substandard policy’.

Medical questions with special reactions

Questions included within this paragraph contain the described reactions. They can be used accordingly or the reaction can be modified via the maintenance program:

Incapable of working

Have you been ill for longer than two weeks?

If the question is answered with 'yes' and no disorder is given in response to this question and the AP is not a child, the application is referred with the comment 'no individual health indication'.

If the question is answered with 'yes' and a disorder is given, the assessment takes the disorder into account.

If the question is not answered, an 'incomplete' reaction is given unless the life assured is a child (age under 18), i.e. the age at proposal is less or equal to CSP signature age.

Healthy and able to work

Are you healthy/able to work?

If the answer is ‘no’ and no disorder is given in response to this question and the AP is not a child, the application is referred with the comment 'no individual health indication'

If the question is answered with 'no' and a disorder is given, the assessment takes the disorder into account.

If the question is not answered, an 'incomplete' reaction is given unless the life assured is a child (age under 18), i.e. the age at proposal is less or equal to CSP signature age.

Reduction in earning capacity

Do you suffer from any reduction in your earning capacity?

Independent of the percentage of the reduction of earning capacity, the application is referred to the underwriter for final assessment. The hint ‘reduction on earning capacity’ is given.

If the percentage of the reduction of earning capacity is missing, the incomplete reaction is triggered.

More disorders

Have you stated all disorders?

If the answer is ‘no’, the application is referred with the comment ‘not all disorders specified’.

Positive HIV test

Have you tested positive for HIV/AIDS?

If the answer is 'yes', the AIDS risk probability is set to 1.0 and the application is declined.

Suicide attempt

Have you ever attempted suicide?

If the answer is 'yes', the application is referred with the comment ‘suicide attempt’.

Hypertension

Do you suffer from high blood pressure?

If the answer is 'yes', the medical report blood pressure is requested. If the answer is missing, the incompleteness reaction is triggered.

Cholesterol

Do you suffer from hypercholesterolaemia?

If the answer is 'yes', the medical report for cholesterol is requested. If the answer is missing, the incompleteness reaction is triggered.

Suspicious signature

If the signature is suspicious, the application is always referred with the comment 'suspicious signature', because it may reveal signs of illness, alcohol or drug abuse etc.

Aids combination

The Aids combination risk consists of the evaluation of the lifestyle questions and the aids risk derived from all application data, based on a probability function.

Aids lifestyle

The Lifestyle questionnaire is asked and evaluated, when the lifestyle questions are used within the user interface definition or the Lifestyle questionnaire is selected in the enclosed document menu. The need of a Lifestyle questionnaire is determined from Limit-DB or depending on CSP aids level lifestyle. If a Lifestyle questionnaire is not available, i.e. not in the list of attached documents or not used in the user interface definition, normal probability check for Aids is done.

The evaluation of the lifestyle questions is not hard-coded in COMPASS. Rules can be defined within this risk level, e.g. if any question of the lifestyle questionnaire is answered 'yes', the application might be referred with the comment 'lifestyle question answered yes’.

If after the evaluation of the lifestyle rules the result is still standard and the life insured is older than 30 years, the reaction is according to the CSP lifestyle question reaction with the following possibilities:

-

refer with the comment ‘check AIDS risk’

-

request GPR

Then no probability check is carried out in addition. If the result is still standard or the age is below or equal 30, the AIDS risk is checked by the system as described below.

Aids risk

The AIDS risk is determined by the probability function, the different application statements are assigned probabilities for or against an AIDS risk.

Foreign travel, nationality

The assessment of foreign travel or nationality is based on country database. The highest aids factor of all single risks is chosen.

Age

If the life assureds age at entry is between 20 and 55 inclusive, this factor is weighted by 0.2.

Premium payer

If a person other than the life assured is paying the premium, the names are different and the persons are of the same sex, this factor is weighted by 0.2.

Occupation

The assessment is obtained from the occupation database. If there is no entry, it is not considered an "at-risk" occupation. The AIDS risk is then downgraded by a factor of -0.2.

Marital status

For single lives assured (incl. separated, divorced) a weighting of 0.2 is applied, for married lives assured the risk is downgraded by -0.2.

Joint lives, HIV infection

If one of several lives to be assured is HIV positive and the names or the postal codes are different, it is assumed this is a business partnership and the factor is weighted by 0.5 for the non-infected person. If the postal codes are identical, it is assumed they are married and the factor is weighted by 1.0.

Sex

Male lives assured receive a weighting of 0.2.

HIV infection

If the life to be assured is HIV positive, i.e. the relevant question in the application is answered 'yes', the risk is weighted by 1.0.

Infectious disease

A disease associated with HIV infection exists where the AIDS value in the Disorder-DB has a value and the attribute maximum duration has no value.

Chronic disease

If the duration is relevant for a disease with HIV infection potential, the attribute maximum duration in the disorder database has a value. The duration of the illness is compared with the entry from the maximum duration field. If this duration is exceeded, the assessment is obtained from the AIDS value attribute.

Sum assured

Any pre-existing cover (as indicated in application and/or from previous business) and the sum assured applied for are added together. If this total sum is just under the value of the CSP examination limit life AIDS, i.e. between 96 and 100 percent of the value of examination_limit_life and no examination is arranged, this factor receives a value of 0.1.

Joint lives, male

Two male lives to be assured whose names are different but who live together, i.e. their postal codes are identical, are rated 0.2.

Beneficiary

In the case of a male life to be assured and male, other or unknown beneficiary, a weighting of 0.3 is applied unless the family name is identical, i.e. suggestive of family members. In the case of a male life assured and a female beneficiary, a downgrading of -0.2 is applied.

In the case of a female life assured and unknown or other beneficiary, a weighting of 0.2 is applied. All other beneficiary situations such as female life assured and male beneficiary are downgraded by -0.2.

COMPASS allows several beneficiaries with different percentages. For the AIDS check the worst scenario is taken into consideration.

Postal code

If the life assured lives in the domicile country COMPASS checks whether the city includes a high AIDS risk. The postal code is compared with entries in the postal codes database. Depending on the CSP aids postal equation the postal code is evaluated, e.g. take only the first two digits. If the city is included in the list, the AIDS risk receives an increase weighting of 0.2. If not, the risk is downgraded by 0.1.

Signature

A suspicious signature may indicate an AIDS risk and is therefore rated 0.1.

Relationship of life (lives) assured / policyholders

In the case of two male names, the factor is rated 0.2. If the names are the same or indicating different sex, a downgrading of -0.2 is applied.

The result from the probability function leads to an assessment of AIDS risks in the following groups, the levels and texts being modifiable:

| Probability result | Reaction |

|---|---|

>= aids level3 |

Decline |

>= aids level2 |

'AIDS suspicion very high' and reasons |

>= aids level1 |

'some indication of AIDS risk' and reasons |

> aids level0 |

'little indication of AIDS risk' and reasons |

It is advisable to refer any result between the aids_level0 and aids_level3 to an underwriter. Depending on the value of CSP aids level lifestyle questionnaire the lifestyle questionnaire is requested additionally, if the value exceeds or reaches the CSP value and has not been requested yet. Where aids_level3 is exceeded, it is advisable to decline.

If reactions of the system are only required in the case of very high AIDS suspicion, e.g. stated by a positive aids test, then the aids level0 should be set to 0.99 and all other aids parameters to 1.00. In this case the text 'little indication for AIDS risk' should be set to 'AIDS suspicion very high'.

Incompleteness

The AIDS assessment takes into consideration information from the application form, which is available from the interface and has no incomplete assessment. If these fields are incomplete the AIDS assessment cannot be done properly. However, in order to enable the system to make a decision even if this data is missing, the system includes a CSP to store any decision to be made if the data (e.g. marital status, sex) is not available. The following data comes from the interface:

-

marital status of life assured

-

name of life assured

-

sex of life assured

The CSP aids default may have the following values:

-

best case

-

worst case

-

take available date

-

assessment of GCR

GCR assessment

name of policyholder is not equal to name of life assured (=worst case)

marital status of life assured is unknown

sex of beneficiary is unknown

sex of account holder is unknown

Best case assessment

name of policyholder is equal to name of life assured

marital status of life assured is married

sex of beneficiary is other than sex of life assured

sex of account holder is other than sex of life assured

Worst case assessment

name of policyholder is not equal to name of life assured

marital status of life assured is single

sex of beneficiary is equal to sex of life assured

sex of account holder is equal to sex of life assured

Special constellations

Currently this risk level does not include any check. Possible checks are e.g. healthy person but younger than 60 and already a pensioner.

Event sum risk

This chapter includes assessments considering the sum insured of same events, independent on the benefit.

Examination limits

Companies already conduct technical assessments of parameters, such as minimum or maximum sum assured, termination age and duration at the time of application data entry. Therefore COMPASS does not perform these assessments.

Examination limits

The medical examination limits are stored in the Medical Limit DB and may be modified in a company-specific way. The Medical Limit DB contains an examination category field, which indicates the group in which the benefits is classified. For example, an examination group can be created for benefit, or just one group for the events Death, IP, LTC, TPD own/similar, TPD any/ADL and Critical Illness. For each group there are database entries with age, sex, marital status, sum assured, policy duration and deferred period (IP) to be adhered to. The age, which is critical for this assessment, is taken directly from the interface field age for examination limit. If several ages apply, the oldest one is taken into account. For the marital status the entries ‘married’ and ‘single’ is possible via the Medical Limit DB. In the Marital Status DB it can be defined which marital status is to be treated ‘single’ or ‘married’, e.g. divorced, widowed. If several examination groups for the same event are transferred, one of these examination groups is used for the assessment and the hint ‘several examination groups for the same benefit group’ is given.

When index-linked benefits have separate examination limits, a separate group must be created. The examination limits for this group should be transferred by the company, e.g. if the general GPR limit is 150.001, the GPR limit for indexed policies is 75.001. The assessment is performed for each life assured.

Medical reports, Lifestyle questionnaires or HIV tests, which are to be obtained in view of the age at entry and sum assured, can also be stored in the Medical Limit DB. The requested ME may include different examinations (e.g. HIV-test, ECG®). However, every individual examination / piece of evidence must be explicitly listed for each limit within the database (e.g. ME / ME and ECG ® / ME and ECG ® and HIV; etc.). General GPRs for IP cover with 4 weeks deferred period should also be stored in the Medical Limit DB.

If no check should be executed for a specific benefits type, then the Limit-DB should not contain entries for the examination group of that tariff.

Establishing the examination limits

The sum that is calculated as follows is used for the lookup in the Medical Limit DB to decide whether and which examinations/documents are necessary:

-

sum of all fitting tariffs from current proposal for AP

-

sums from existing insurances at the own company according to CSP own previous covers included for medical limits only for aids

-

sums from existing insurances at other companies according to CSP other pre-existing covers included for medical examination limits

-

bonus (optional – can be changed by Gen Re)

-

sums insured applied for simultaneously (to be recognized at the field ‚acceptance result’ for previous insurances)

If the CSP own pre-existing covers included for medical limits only for aids is set and the requested examinations do not contain HIV then the system adds the correspondent sums to check only if HIV is necessary.

In the case of single-premium policies, the sum is reduced by the amount of the single premium, unless it is not a IP or LTC applied for. Where the IP benefit is to be reduced, determination of the relevant evidence to be obtained according to the medical examination limits will be based on the reduced benefit, if the CSP consolidate reduced is ‘yes’.

Specialities for some events

TPD

Examination limits are checked for TPDown/similar and TPDany/ADL separately.

WOP

Examination limits are checked for all WOPown/similar and WOPany/ADL separately. The sum to be checked is derived from the related premiums.

IP

Examination limits are checked for all IPown/similar and IPany/ADL separately. Where several IP benefits have been applied for simultaneously, the sums assured of those IP with shorter or equal deferred periods are added together.

The same procedure applies for previous insurances, i.e. only those ones are added to the one applied for with a deferred period shorter or equal.

Request of evidences

If various pieces of evidence are required for various events, such as Life and IP, the total evidence will be required.

Requesting evidences as a result from the limit check including previous insurances can be avoided when the current sum applied for is very small. The CSP minimum of annual benefit for requesting evidences / minimum sum for requesting evidences includes the benefit specific limits from which on the evidences should be requested. If the sum assured is below this minimum but the evidences are requested caused by previous insurances, the system will refer with the comment ‘check request of MEs because of small sums’.

Financial limits

All checks for financial limits are processed using the financial limit database. These checks are described in the chapter Benefit specific total sum check.

Sum needs assessment

This chapter includes the IP needs analysis related to the annual benefits for the same event. These checks are described in the chapter IP need assessment.

Legal AP

Signatures

The incompleteness check for the assured person’s signature is processed, if it is needed:

| Age | Signature requested |

|---|---|

Age < CSP signature_age |

signature of legal representative of AP |

Age >= CSP signature_age |

signature of AP |

A typical value for CSP signature age might be 18 years. COMPASS will check the age on the day the application form was signed.

Signature health declaration

The signature for the health declaration is needed, if the age at proposal is less or equals the value of CSP signature age. If the signature is not available it is requested from the client.

Minor assured persons

The benefit group related entries in the financial limit database can be used for age and sum insured related checks of minor assured persons. So every company has the flexibility to decide up to which sums minor assured persons are acceptable. Possible explanation texts for referral are: 'insured is a minor, acceptance guidelines not adhered to’.

Benefit risk

This risk contains assessment rules for benefits, which can contain more than one event. Those benefits are very company specific and therefore only very basic rules are included in the delivery. Special rules for joint lifes benefits with a death risk for each applicant can also be defined on this level.

TPD own/similar and TPD any

If the result of TPD own is not ‘decline’ and an exclusion clause is necessary and the result of TPD any is decline, then the result for TPD any is set to ‘refer’ and the comment ‘check TPD any for possible exclusion clause’ is given. The result for TPD own remains as it is.

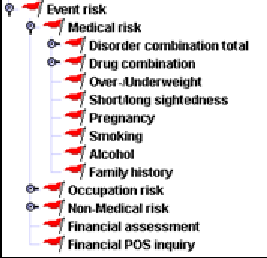

Event risk

The event risk consists of the medical and non-medical risk, occupational and financial risk. The results of all areas are consolidated in this chapter.

The result is the 'worst' result of all individual risks.